Stepping Back to Reposition: Is it Time to Re-evaluate IA’s Value proposition?

If it’s been said once, it’s been said one hundred times: the current pandemic and its impacts are unprecedented.

In one way or another, all organizations have been affected, given the profound social and economic disruptions COVID-19 has caused. To adapt, organizations may need to rethink part, or all their current business models to maintain their position in the market or to at least be adequately prepared to seize new opportunities. Along the same lines, the internal audit function must also take advantage of this opportunity to step back and review its strategies and ways of doing things in order to stay relevant and provide value-added services. The Chief Audit Executive has a great opportunity here to assume leadership in this regard.

Many agree that this crisis is not only a point of no return, but an opportunity to innovate. A new reality is emerging, and it’s time to adapt. The same is to be said for the role of internal auditing; it will certainly not be the same in the future as it was pre-pandemic. To adjust to the “new” normal, Chief Audit Executives need to consider the following questions:

- What will be the external and internal changes that will impact our organization?

- How will these changes affect our organization’s strategies and business model?

- How should internal auditing adapt to these changes?

- How can internal auditing remain relevant?

- What should internal audit do in the short to medium term?

- What are the relevant emerging risks to consider?

- How can I anticipate what the economic rebound and the future will mean to our business?

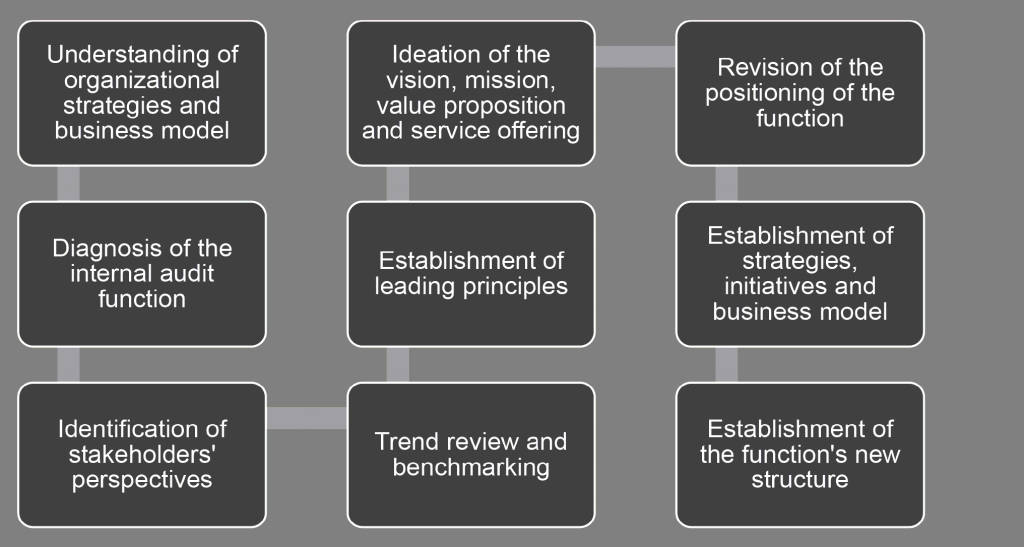

One of the best ways to find answers to these questions is to embark on an exercise to revise the current strategic plan of the internal audit function or even, to prepare a new one completely.

Such an exercise allows for in-depth introspection, identification of stakeholders’ perspectives and current trends. It provides a vision, mission and strategic objectives that can be translated into a number of initiatives over the next few years. Specifically, a strategic plan could include the following elements:

The preparation or updating of such a plan requires the involvement of all members of the internal audit function and a strong commitment to change the status quo. The internal audit innovation component should play a prominent role in this exercise to identify new ideas, new ways of doing things, or simply different ways to improve the existing situation.

Several aspects need to be challenged to ensure that internal audit functions can seize opportunities to do better, more effectively, and with continued relevance.

The functions are also called upon to reflect on concepts of agility and to introduce positive elements of agility into their methods, starting at the strategic planning stage. When looking back on the strategic plan, why not use the information inputs available to enhance or modify the initiatives previously identified and work in tune with the organizational reality!

The strategic plan is the pillar that will enable all members of the internal audit function and its stakeholders to rally around clearly established common goals. The internal audit strategic plan is the backbone for the preparation of an audit plan that will be supportive of the organization. Alignment of the strategic plan with the audit plan is essential. Without a documented strategic vision, the audit plan loses its relevance.

How can Richter help?

- Diagnostic of the internal audit function;

- Preparation of the strategic plan;

- Benchmarking exercises;

- Input toward best practices and trends;

- Analysis of the impacts of the pandemic crisis on your strategic plan;

- Training, working sessions and workshop facilitation.